U.S. Bitcoin Family Estate Readiness

The first calm conversation about Bitcoin continuity—for normal families.

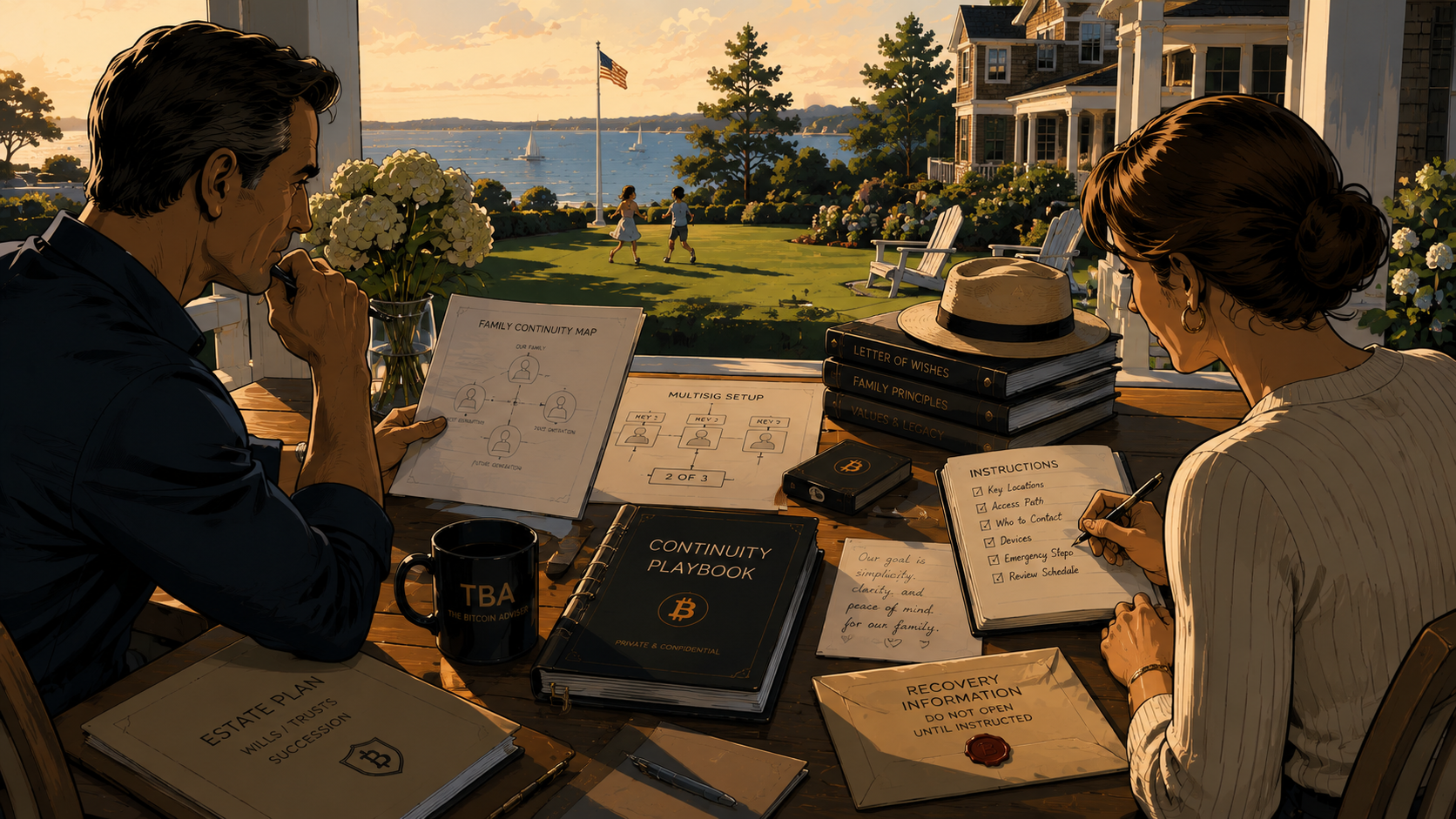

Legal papers alone don’t unlock Bitcoin. A short walkthrough shows what you have, what might be missing, and what to bring to your attorney or CPA.

About two minutes. Stays in your browser. No signup.

Most plans assume someone else can move the money

With a bank or brokerage, institutions and court orders create a path. Bitcoin is different: it is keys and instructions your family has to be able to find and use. The best time to line that up is while life feels ordinary.

Your professionals, plus the practical side

Your attorney handles legal advice. Your CPA handles tax. We help families make the operational side—where things live, who would do what, and simple rehearsals—something real people can follow when stress is high.

A simple family continuity walkthrough

Nothing here is submitted automatically. Your answers stay in this browser unless you choose to reach out.

About your household

Try a starting picture: · · ·

If you want more context after your snapshot, the sections below use the same plain language—no need to read them before the walkthrough.

Most People Miss These Basics

You’re not behind. Most families skip the simple things that matter when life gets real.

The people

Who will handle money and kids if you can’t? Executor, backup trustee if you use a trust, medical decision-maker, guardians for kids—they need to know more than their title; they need to know what you actually intended.

The paperwork

Will or trust, powers of attorney, and a simple list of where things live. Your lawyer drafts the official version; your job is making sure the right people could act without guessing.

The Bitcoin part: A judge can give someone authority on paper. They still need a safe path to the keys and a clear “what to do next.” That is why a short written guide your family can follow matters so much.

Easy things to forget: no backup person named, no list of accounts, kids’ money treated like everyday checking, retirement Bitcoin handled like a phone app.

What Good Usually Looks Like

There is no single “right” shape for every family. Strong setups tend to share a few habits: the right people are named, the paperwork matches real life, and someone other than you could find instructions without panicking. When Bitcoin is involved, “good” also means your family could describe—at a high level—where savings live and who would help them use it responsibly.

Many families also keep a simple inventory, a short continuity note their attorney has seen, and an occasional check-in so a plan on paper still matches devices and backups at home. Your attorney will tell you if a trust or other structure fits; this page is only here so the practical side does not get lost.

The goal is not perfection. It is reducing confusion on a bad day.

Where Your Bitcoin Lives

Just like you might not keep every dollar in one checking account, many families keep Bitcoin in more than one place on purpose—personal spending, longer-term savings for kids, a business, or tax-advantaged accounts. That is normal, and it is easier on everyone when each place has a plain-English “why this exists.”

A good rule of thumb: each place has someone who knows it exists, what it is for, and how to get help without sharing more detail than necessary.

Examples families use: personal stack; savings held for children or future generations; business treasury; tax-advantaged accounts with their own rules.

FAQs

What if my family is not technical?

That is normal. The point is not turning anyone into an engineer—it is clear writing, a sensible folder structure, and one or two rehearsals with the people who would actually step in. We help you translate the technical side into plain language and checklists your family can follow, alongside your attorney and CPA. You keep the keys; we help you make the path legible.

Why more than one setup?

Different slices of life—personal, trust, business, retirement—often need separate setups for clarity, taxes, and who is allowed to act. Each can have different owners, rules, and backup plans.

Why do SDIRA and HSA differ?

IRAs and HSAs have special tax rules from the IRS. They can hold Bitcoin but work differently than your personal vaults. Your CPA and plan administrator guide those details.

Do kids need their own keys?

Usually not when they're young. A trust or similar structure holds the Bitcoin until they reach a certain age. Your attorney designs how that works for your family.

What if one spouse dies?

Personal vaults with joint control may pass to the survivor. Trust vaults follow the trust document—the backup trustee steps in. The key is that everyone knows where the keys are and how to use them.

What does an inventory or runbook include?

An inventory lists your vaults, key holders, and where things live. A runbook gives your family step-by-step instructions to recover or transact. We help you document both—you always keep the keys.

How does TBA fit in if you don't hold our Bitcoin?

We provide simple frameworks, checklists, practice drills, and help connect you with great attorneys and CPAs. You hold the keys; we help you get organized so your family can act when needed.

Part of our free U.S. resources. You might also like Bitcoin Estate Planning 101, the Bitcoin-aware will generator (draft for counsel), and Simple Governance Tips.